Vietnam cold

storage market: huge potential but fierce competition

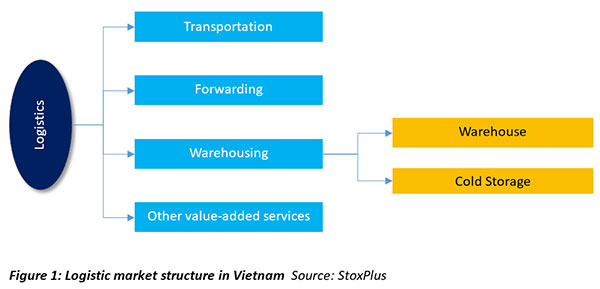

Cold storage

is classified as climate control logistics which refers to a system

controlling the temperate and humidity with the purpose of increasing the

storing period for particular categories of goods.

Cold storage

can be segmented into three main categories namely deep frozen (-28 – -30oC

for storing seafood), frozen (-16 – -20oC for storing meat), and chiller (2 –

4oC for vegetables, fruits and flower).

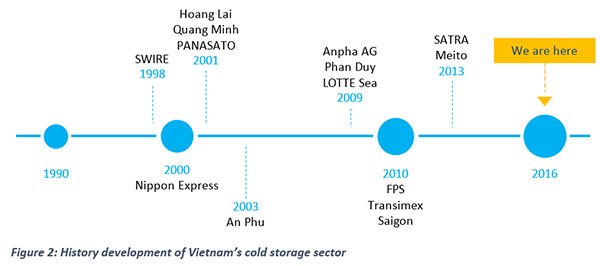

The cold

storage market in Vietnam has a short development history of 20 years. The

first commercial cold storage was built in 1996 by Konoike VinaTrans, a

logistics joint venture between Konoike transport Co. Ltd (Japan), Vinatrans

Co. (Vietnam), Vinalink Co.(Vietnam), and Vinafreight Co. (Vietnam).

Subsequently

in 1998, Swire Cold Storage from Australia followed Konoike to build one of

the most modern cold storages to date in Vietnam. The market started booming

in 2007 with the construction four cold storages in the same year. Hung Vuong

built two storages with a total capacity of 40,000

pallets to

meet its in-house storage demand as well as to provide storage services for

other seafood and retailer companies in the market. Both local and foreign

cold storage providers have become interested in the market since then.

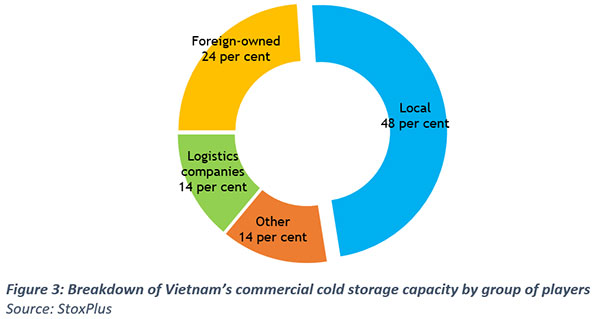

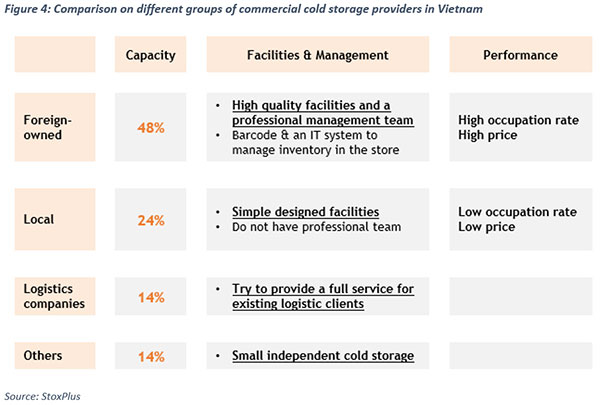

As surveyed

by StoxPlus, major commercial cold storage providers are mainly situated in

the South due to high demand of this region and can be classified into four

main groups of players namely local, foreign-owned logistics companies, and

others as Figure 3.

Despite of

dominating the market in terms of designed capacity, local companies are

considered the second tier. The leading local companies are Hoang Lai, Hung

Vuong, SATRA, and Phan Duy. Of which, two leading companies, namely Hung

Vuong and SATRA were the first to operate cold storage facilities to serve

their in-house demand. However, local companies’ cold storages are equipped

with standard facilities and simple designs. Some cold storages even do not

even have racks for storing.

Meanwhile,

foreign-owned group lead the market by leveraging professional management and

modern facilities. Established in 1998, SWIRE was one of the first

foreign-owned cold storage providers penetrating Vietnam with professional

management as well as modern facilities. Other foreign-owned providers are

Lotte Sea (2009) and Preferred Freezer Services (2010). Foreign-owned

commercial cold storage providers are the market leaders in quality and

management services with a diversified portfolio of clients and prime

location.

Huge

potentials from Vietnam commercial cold storage market According to

Vietnam Cold Storage Market 2016 by StoxPlus, cold storage is one of the most

potential logistics segment for growing in Vietnam, since Vietnam is an

agriculture economy. Few foreign and local companies tapped in this segment

and none of them provides the whole chain service.

Four main

sources of cold storage demand include seafood, meat, fruit and vegetables,

and grocery retailing. Of which, seafood export and grocery retailers are

expected to be drivers for cold storage demand growth in the future thanks to

a number of free trade agreements (FTAs) signed in 2015.

In

particular, the zero import tariffs in large markets like the US, Japan, and

Canada will create a huge advantage for Vietnamese exports. This will lead to

increasing logistics demand including cold storage for preserving the goods

serving for importing and exporting purposes.

Besides,

modern trade is of increasing importance and giant, international retail

corporations have plans to penetrate the Vietnam market in the near future.

Vietnam is expected to have about 1,200-1,300 supermarkets, 180 shopping

centers, and 157 department stores by 2020. Distribution centres including

cold storage will also increase in number and capacity to fulfill the demand

from the development of supermarkets.

It is noted

by StoxPlus that each end-use sector posts different requirements and cold

storage demand outlook. The market is expected to be more competitive with a

few cold storage investment projects developed by both local and foreign

investors. Particularly, the biggest investment is the 50,000 pallet cold

storage facility in Song Hau Industrial Zone in the Mekong Delta province of

Hau Giang. The project is in the initial phase and developed by Minh Phu and

Gemadept Corporation with the total investment capital of $46.1 million. When

completed it will be the largest cold storage facility in the Mekong Delta.

Besides, the

Cool Japan Fund established a joint venture with Japan Logistic Systems Corp.

(JLS) and Kawasaki Kisen Kaisha Co. Ltd, (“K” LINE) to build a $15 million

refrigerated storage facility in the Ho Chi Minh City suburbs.

As such, to

seize the upcoming opportunities in Vietnam cold storage market, it is argued

by StoxPlus that existing players as well as foreign investors who want to

penetrate in Vietnam market should identify the key segments and appropriate

sale and marketing plans to catch the trend.

By Minh Hai, VIR

|

Thứ Năm, 26 tháng 1, 2017

Đăng ký:

Đăng Nhận xét (Atom)

Không có nhận xét nào:

Đăng nhận xét